|

| Short term target 31.75, if it takes out resistance at 30 |

|

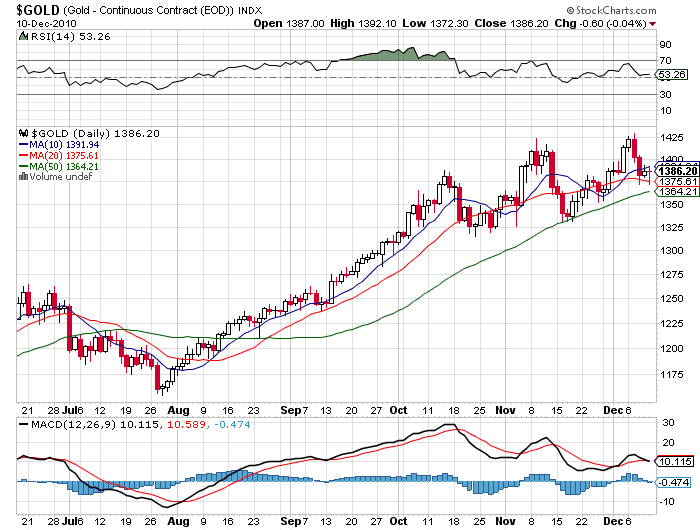

| Gold still has serious work to do see major resistance line its going to take a big fall in the dollar to get this move higher. |

The dollar index is down a percent this week if we see the UUP fall below 22.8 i think gold will breakout at that point and silver will we over 32. Something major has to happen for this to play out but the charts are signaling something to come soon.

The SPX Index there were 262 Advancers/210 Decliners. On the NYSE 3,147 issues were traded with 1,950 advancing issues and 1,121 retreating issues, a ratio of 1.74 to one advancing. There were 189 new highs and 17 new lows. The five day moving average of New Highs is 170 while the five day moving average of New Lows is 14 and the ten day moving average of Net Advancing is 329. The Net Advancing data indicates a bullish trend.

Advancing volume was higher at a ratio of 1.59 to one. The closing TRIN was 1.1 and the final tick was -8. The five day average of TRIN is 1.11 and the ten day average of TRIN is .99. The NYSE Composite Index gained 0.38% today while the SPX gained 0.1%. For the NYSE, relative to the previous 30 session average, volume was -47.27% below the average. Of the last 15 sessions 3 sessions ended with volume greater than the previous rolling 30 day average volume. Of the last 30 sessions, 18 sessions ended on a positive tick, 5 of last 10. For the SPX, the day's volume was 48.5% of the average daily volume for the last year. Volume was 56.4% of the last 10 day average and 92.3% of the previous day’s volume.

Breadth today was substantially stronger than a one point index gain suggested. But advancing volume was weaker than advancing issues. So we don’t believe that today’s breadth tells us much.

Total tick for the day was 205,000 and the average tick for the day was 132. There were 3 ticks greater than 600 and 0 ticks more extreme than -600. There were no ticks greater than 1000 and no ticks more extreme than -1000.

|

| Headed to 22.8 |

There were only three ticks more extreme than 600 all day. But almost 80% of all ticks were positive. Looking at the Nightly Breadth Indicators reveals what we have seen the last several days; sluggish almost nonexistent trade action with the likelihood of a few more days like this.

Short Long Bond, Long Miners Metal and Uranium, Long Precious Metals, Sold AIB for 21% loss, hold IRE 22% gain, Close out CRUS for 5% loss today. Otherwise no change.