Over the past few weeks I have posted about the breakdown of the US long bond. This has serious implications for all of us. (See yesterday's post for charts)

Judging solely by the price action in both the Ten year and the long bond, the Fed’s QE program, which was designed to hold down long term interest rates and thus spur lending particularly in an attempt to generate activity in the real estate sector, has proven to be a failure. The exact opposite of what was intended by the FED is happening, and when you combine that with a huge number of houses available due to the wave of foreclosures and it is difficult to see this turning around any time soon. The plan was to artificially force down longer term rates through the purchase of Treasuries which would spur bank lending and consumer spending and business growth, and hiring etc.

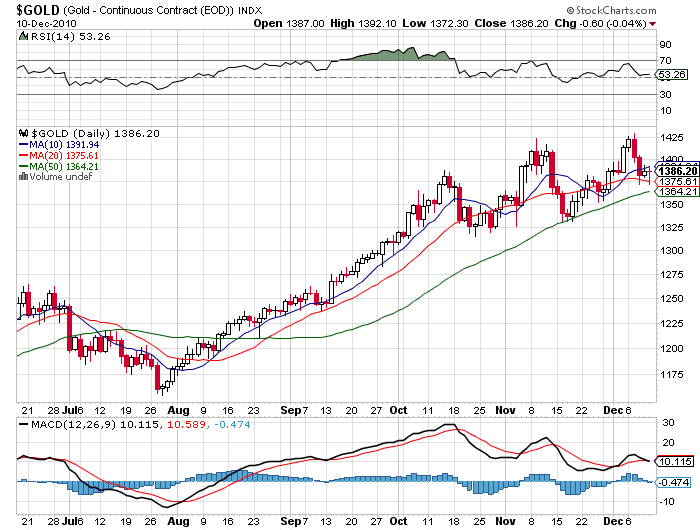

How that is going to happen when the rates are going in the opposite direction? The bond holders are speaking loud and clear, they are not going to hold these bond because they see the inflation, charts don't lie.The simple fact is that the CCI (Continuous Commodity Index) is soaring now has fully captured the attention of the bond market and unless the easy money policy is withdrawn, there will be never ending wave of selling, so short the long bond or go long TBT or TBF.

The long holdout on the FOMC, Governor Hoenig has had it right all along he has been the dissenting voter in the FED he has voiced his strong opinion on the potential for strong inflationary pressures as a result of QE. The Fed has has kept the stock market propped up and and the cheap money is finding a home for now in stocks. The other effect its having is over inflating commodity prices and that is a great cost to us all and especially to the unemployed or those just getting by.

The next troubling thing I am seeing is that rates are rising in the 5 year, which means that the government is going to have to borrow more and more on a short term basis in order to fund its ballooning budget deficit and its rising entitlement costs if it wants to keep its borrowing costs low. That may work for a while but the fact is that a nation so deeply in debt as we are we are now at the mercy of market forces that could drastically force yields upwards, meaning the cost of carrying this mountain of debt grows larger with each passing month. In other words, our creditors are going to be demanding more money to support us. I don't know how this can play out without it getting ugly.

The speed at which the bond market is breaking down is startling. The problem with markets which begin to act like this is that often times that selling begins to feed on itself and a frenzy to unload commences. It may or may not happen to the bonds but the risk is there. Quite frankly, there is only one line of support I can see on the price charts near the 119 level that is standing between the long bond and a drop below 115. If it gets down into that region, things are going to get really scary.

Having experience with the tech bubble, the housing bubble, the mortgage and financial meltdown has given me a different way to look at the information I am fed by politicians and media. Seemingly I wasn't the only one blindsided by those events, don't get fooled by action in the SPX, its not about a growth cycle, or jobs or prosperity worldwide.

Long TBT